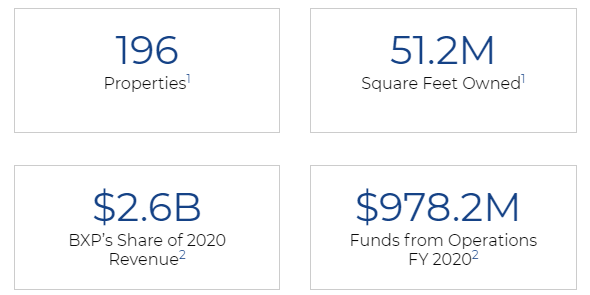

Boston Properties (BXP) is an office REIT with a portfolio of 196 properties and over 51 million square feet. The portfolio concentrated in five markets – Boston, Los Angeles, New York, San Francisco and Washington, DC.

BXP has an existing $2.2B pipeline of developments that is 87% pre-leased and is projected to add $218 million of Cash NOI upon stabilization. Also, the company has an additional $700 million of near-term development/ redevelopment starts, largely focused on life sciences.

We recently caught up with the company’s CEO, Owen Thomas, to discuss the macro-level environment, earnings, growth, and the “all-important” dividend.

Enjoy the video (19 minutes) and transcript below:

Interview Transcript:

Brad Thomas:

Hi everyone. This is Brad Thomas with The Ground Up, but I’m back again with another CEO round table interview. Today we’re going to move over to a really interesting sector, the office sector, and I’m honored and really pleased to have Owen Thomas with me today. Owen is the CEO of Boston Properties. That ticker symbol’s (BXP). Owen, it’s good to see you today.

Owen Thomas:

Brad, thank you for having me. I appreciate being here very much.

Brad Thomas:

Full disclosure, we do share the last name. We may be related. We may not. I’ve got another CEO, John Thomas, and we always joke about this from Physicians Reality. So one thing’s for sure, we have a great last name.

Owen Thomas:

That’s true. And both Southern so.

Brad Thomas:

Exactly, exactly. Listen, let’s dive into the office sector and specifically, urban, the gateway office market. We’ve obviously been covering the office sector for quite a while, but obviously, there’s been a significant meltdown as it relates to COVID. So let’s look at what’s the state of the market? How do you see things today? You’re physically in New York City where your company is based. How do you see the office sector today?

Owen Thomas:

Yeah. Well, I think, Brad, in all fairness, I wouldn’t use the word, the term, meltdown. So let me explain what I mean. First of all, we have 52 million square feet of office space. The company we’re in the major gateway markets. We tend to have the high quality buildings in our markets. We’ve been collecting throughout this crisis 99% of the rents from our office customers. Our weighted average lease term in the portfolio is over eight years.

And we have named firms in the legal profession, banks, asset managers, technology companies, and life science companies. So they’re paying their rent. They’re not using their space, generally. The census in our buildings, which is a measure of occupancy, on average is probably around 10%. And it is starting to rise weekly, although we’re still below peaks that we saw in the fall.

And then in terms of… But we’re doing leasing. Last year, we leased 3.2 million square feet of space within a weighted average lease term of over eight years. That was 60% of our typical transaction volume in a year. And our markets transaction volume was about 40% of normal. So we outperformed the market, and there is still a market.

We’re having tours every day somewhere in the company, and people are looking at space. Market rents, it varies. I would say New York and San Francisco may be today on a net effective rent basis. It’s down about 10%. And I would say, it’s better than that elsewhere. And we’ve got pockets of the company, particularly those pockets around life science, where I’d say rents are probably higher as a result of COVID.

The big question is the reopening. We’re definitely seeing it. It’s palpable. As you can see, I’m here in my office in New York. It’s palpable in New York City. The restaurants are active. It’s warmed up here a little bit. Retail is more active. Street life is coming back.

I think office will be a little bit of a lag. Employers will not start mandating return to work until more people are vaccinated and the infection rates are lower. We anticipate that to happen this summer. And I do think Labor Day will be a tipping point for this, because we have a culture in this country of back to school, back to work post Labor Day. And I do think a lot of employers are going to focus on that Labor Day weekend as a marker for returning to the office.

Brad Thomas:

Oh, you mentioned the 99% rent. I know you do have some ground level retail in some of your towers, how has the retail today in terms of some of those trophy assets that you own?

Owen Thomas:

Yeah. The collections there have definitely been lower. We do have certain types of retail that’s performed well. For example, we have the iconic Apple Store here in New York that you see photographed. It’s right near Central Park, right in front of the GM Building. Obviously, that’s been Apple as a company is performing well and that store’s performing well, but we do have service retail near many of our office buildings.

So these would be restaurants, in some cases smaller shops. And those businesses have struggled through COVID, and we’ve worked cooperatively and supportively with them abating rent, differing rent. We could to try to make sure they stay on their feet as best they can and, hopefully, successfully reopen in 2021.

Brad Thomas:

Can you talk a little bit about your I guess growth platform and, specifically, I guess, starting with your development pipeline and what impacts have you seen with that in terms of COVID?

Owen Thomas:

Yeah. So we do have a strong growth story and I think investors are starting to understand that our stock is up quite a bit just in the last week, but it’s still way below where it was in February of 2019 before the pandemic. And I would say the growth is in three areas.

First, we lost about $130 million of FFO from variable income streams. So we have a big parking garages at the Prudential Center in Boston, at Embarcadero Center in San Francisco. We have a lot of individual parking at our buildings in Washington, DC, and that evaporated. If people aren’t coming to the office, they’re not parking.

So more than half of that 130 million is parking. And think about it, when people come back to the office, it’s all going to fill back up again. And also I could argue maybe we’re going to be more parking, because people are going to be reluctant to get on a train and use public transportation. So I think that’s going to come back rapidly this fall.

And then another big chunk of that 130 is retail. And I described what we’ve done there. And I do think people are going to be coming back to the stores and restaurants. Again, last night, just here in New York, the governor has increased the occupancy limits.

And with warm weather, there’s a lot more outdoor dining. So you feel that happening. And then we do own the Cambridge Marriott Hotel, and that’s also was closed. It’s now reopened, but the income’s way down from that. So first growth driver, all the least variable income streams are coming back. There’s no doubt about it, and I think they could come back fairly quickly.

And then-

Brad Thomas:

What’s second?

Owen Thomas:

The second thing I just want to mention, Brad, is we do have a development pipeline that is about three and a half million square feet, 2.2 billion of investment. It’s 88% pre-leased to franchise names like Fannie Mae, Wilmer Hale, the law firm. We’re billing Marriott’s headquarters, for example, and this pipeline will be delivered over the next three years onto our balance sheet.

And it adds 3.8% growth to our FFO, the CAGR, so annual growth, 3.8% external growth driver from that pipeline. So again, we have to finish leasing it, but these projects are already successful and we’ve been leasing it. We did a big deal with VW North America, put their headquarters in the building in Reston, which brought up its occupancy.

And then this week, the last piece of the growth driver is new developments that we’re starting. And believe it or not here in the middle of COVID, this week we announced the launch of a half a billion dollars of new developments. They’re all geared towards life science. So we are redeveloping an office building in Waltham. It’s a lab.

We’re building a new lab building in Waltham ground up, and we’re doing another ground-up development at our gateway joint venture in South San Francisco. And these projects we think will generate an 8% stabilized cash yield all costs. And these assets stabilize trading in the four and five cap rate range. So there’s a nice profit there for shareholders. So we still even in the middle of COVID have some strong growth drivers that are going to be great opportunities for shareholders.

Brad Thomas:

Owen, when you look at now we’ve all of us have been through a year of this pandemic. And when you reflect on that and look at your portfolio was really well positioned. None of us knew this, I still call it a Black Swan Event, but you not what you want. But in terms of your geographic focus diversification, you’re not just New York City. In terms of your product mix, you’re not just office. Like you said, you’ve already got that sliver of life science and now growing that even larger. And so you actually, I think, are in a much better position than many of your peers who were in say one specific market or one specific product type. Can you touch on that a little bit?

Owen Thomas:

Yeah. Yeah. I think you’re right. I think the thing I would focus on too, that I think is going to be important in the future is the quality of our portfolio. Because I think going forward with now a better enabled workforce at working from anywhere or working from home, employers are going to increasingly be looking for ways to entice their employees back to the office. It’s got to be easy. It’s got to be productive.

It’s got to be fun. So having high quality space near public transportation with amenities, with a high quality landlord that’s focused on the occupant’s health security, these factors are going to be increasingly important for us competing in the future. And this is one of the things I think where we have an advantage.

I also think that the… You have to look at it by industry. And I do think tech and life science are going to continue to be big drivers of the growth in office demand. And we have increasingly moved our portfolio to create product geared for that customer base. And I think that will only accelerate pre COVID. And in addition to the growth drivers that I mentioned, we also have a 15 million square foot Land Bank that we control in places like Cambridge, in Waltham, in South San Francisco, in the city of San Francisco, where there is going to be significant tech and life science demand.

Brad Thomas:

Do you see a… I guess, have you telegraphed any types of how large do you anticipate moving that dial in life science? Is that something that could be a larger, more significant part of your business model or you have any tiny target exposure in that sector?

Owen Thomas:

Yes. Well, we have today, if you look at the life science tenants that are in our income stream, it’s about five or six percent of our total revenue. And if you look at the land that we control and the redevelopments, the office buildings that we own, that we think we can redevelop to life science, I think that represents from memory about another four or 5 million square feet. And that’s just simply what we control.

And honestly, that’s really important because these three projects that I just mentioned, one of the reasons why the economics is so strong on those is because we already control the raw material. There’s a lot of capital that’s moving into life science today. So people are paying pretty full prices for buildings and for land to create life science projects.

Whereas in our case, we have the experience. We built the Broad Institutes Labs. We built the labs for Biogen. We just successfully did a redevelopment at 200 West Street in Waltham, where we converted an office to a lab and leased the entire thing to translate [inaudible 00:13:12]. So we have the experience to do it. And then in addition, we have a lot of the raw material that we need to continue that pipeline.

So I think it could grow. Again, it’s hard to say, because you never know exactly what’s going to happen with the rest of the company, but if we’re six percent now, I think that could double over time. Again, we’re a developer. So if we went out and tried to buy these assets, the yields would be four to five percent. And if we build them, we think that the yields are going to be over seven. So it’s a much higher yield, but it takes longer to bring that income into the company, because it takes several years to build these projects.

Brad Thomas:

Yep. So looking at your other growth driver, I guess, being your balance sheet and cost of capital, arguably Boston Property has a fortress balance sheet, that BBB S&P rating. You really maintain a very disciplined capital stack, at least over the period I’ve been covering the company. Your dividend is still well-protected, even though we did, to your point, lost some income, some earnings in ’20.

We’ve got analysts forecasting a clawback of about five percent growth in ’21, eight percent growth in ’22. And you probably don’t even look at analysts. I don’t know if all their estimates, but I do. And I look at ’22 and I don’t think there’s many analysts that are going to go out that far. But for that group, I see 12% growth. So really strong growth recovery, at least from what the analysts are telling me.

But how are you utilizing that balance sheet? Obviously, your equity multiple has moved, so we’re encouraged to see that recovery underway in your terms of your pricing. But how are you equipped to capitalize on all of these growth opportunities you just outlined?

Owen Thomas:

Yeah. Well, we just did an $850 million unsecured deal at just over two and a half percent. It was 11-year deal and it just over two and a half percent. And by the way, it was in green bonds, so we got some benefit from that. We have a tremendous amount of liquidity. We are in… And I think… And we also, by the way, have joint venture partners, private equity joint venture partners that want to join us for acquisitions.

So as you’re suggesting, Brad, we have a significant amount of investment capacity that we can use in the marketplace. The other thing that we’re doing is we always sell assets too. So last year we sold $550 million of real estate. These are either assets that are non-core or assets that are not growing necessarily so rapidly, and we’re getting an interesting cap rate. And so that creates liquidity as well.

Although be aware. Sales often create special dividend requirements. So it’s not a 100% efficient way to raise capital. And so the way we’re investing it is first the deals I just described. There’s three life science developments. And again, we’re investing half a billion dollars into those. I hope and think there will be more life science developments.

We have this 15 million square foot land portfolio. We have put on pause our office development subject to pre-leasing. So we wouldn’t launch a speculative office project.

If we could get a pre-lease on some of our sites, then we would launch those projects. And then we’re looking for acquisitions. We have not seen much what I’d call distress, in class A office in the cities where we operate yet. But we have gone through a pandemic and we have our own balance sheet, and we’d have these sophisticated financial partners that I mentioned that want a joint venture with us to make acquisitions. And we’re always looking for deals.

Brad Thomas:

Great. And in terms of, I guess last question I want to touch on, Owen, is dividend policy. You did have a modest cut in the great recession in 2008-2009. It was very modest. And actually looking at that period of time, you had about a 25% decline in FFO in 2008 with a slight, again very slight dividend cut in 2009. So 2020, we’ve seen about a 10% decline in FFO, but obviously your dividend was in much better shape in terms of your pay out ratio.

So it looks like one thing you’ve done over the last 10 years, very obviously, is really prepared for that next event, which we didn’t know it was going to be a global pandemic. But in fact, you’ve been able to weather this storm pretty, pretty darn well, given the fact that you’ve maintained a very disciplined balance sheet and a low payout ratio. So how do you, I guess, sum of all those parts, how do you feel about that payout ratio today in that all-important dividend?

Owen Thomas:

Yeah. Well, our goal is to have a stable and growing dividend. And as you said, Brad, our income stream… You hear all these things about office, and the stock did go down rather materially as a result of the COVID pandemic. But our income stream was down 10, 15%. So we’ve kept the dividends stable. By the way, as you mentioned, our rating, we’re Baa1 Moody’s rating, which is the highest, the best rating that’s out there for the office real estate companies.

And then the other thing that we’ve been doing, the dividend… Our net income has come down. So it’s actually given us capacity to sell more assets, because that gain we’re sending out as part of the regular dividends. So in a way we’ve almost raised more cash as a result of, if you think about it that way, as a result of keeping the dividends stable. So that’s our goal. And as I described in your first question, we’ve got a lot of drivers to get that FFO per share and that income higher in the quarters ahead, whether it be from the recovery play, as well as the external developments that we’ll be bringing online.

Brad Thomas:

Right. Well, Owen, I want to thank you for your time. It’s been very, very helpful to me, and I’m sure our audience as well. And I look forward to circling back after the first quarter as we continue this recovery moving forward. So I thank you again for your time.

Owen Thomas:

Great, Brad. Thanks for having me. All right. Best of luck.

Happy Investing

Brad Thomas is Senior Research Analyst at iREIT and CEO of Wide Moat Research LLC. With over 30 years of real estate experience, he is also long-time Editor of Forbes Real Estate Investor, a monthly subscription-based newsletter that dives deep into the vast world of profitable properties, and since 2021, he has served as an adjunct professor at New York University.

Thomas has also been featured on or in Forbes magazine, Kiplinger's, U.S. News and World Report, Money, NPR, Institutional Investor, GlobeStreet, CNN, Newsmax, and Fox. And he was the #1 contributing analyst on Seeking Alpha in 2014, 2015, 2016, 2017, 2018, 2019, 2020 and 2021 based on both page views and number of followers.

Thomas is the recently-published author of The Intelligent REIT Investor Guide (2021), co-author of The Intelligent REIT Investor (2016), and he wrote The Trump Factor: Unlocking The Secrets Behind The Trump Empire (2016) - all available on Amazon.

Thomas received a bachelor of science in business/economics from Presbyterian College and is married with five wonderful kids.